Global Britain

Exporting Construction

Most of the time I look inward at the UK, or London, but this piece is outward looking, with focus on the potential exporting of our skills and services on the world stage. Mace Consult have issued a report which assesses the opportunity, so I’ve taken a look and extracted the highlights. It’s good to change perspective every now and then.

While writing this, I couldn’t help but wonder… if the ‘pull’ to deploy services oversees is the need that these countries have, perhaps the ‘push’ is the friction we face in the UK system. Maybe such friction explains why businesses trading internationally are apparently 20% more productive (see below)?!

The Opportunity

Construction services are only a small percentage of total exports at 0.4% (up from 0.2% in 2010), however the share of the global construction market delivered by UK firms has increased from 0.5% to 6.4% in the last twenty years.

The UK's construction services sector has experienced significant growth, with a 53% increase in value in the last three years, amounting to £4.6 billion. And the demand for major construction is expected to rise due to 1) population growth coupled with urbanisation, and 2) sustainability needs as everyone scrambles to get close to Net Zero targets. Mace say this represents a £400 billion annual export opportunity for the UK and their Construction Partner Index ranks 78 countries to help identify the international partners with most potential.

The report explains that the ‘export opportunity’ matters for three key reasons:

export supported jobs are higher value than those domestically, paying around 7% more. And they provide resilience and a spread of risk.

businesses trading internationally are 20% more productive.

helping middle and low-income countries deliver projects ultimately benefits everyone.

It highlights that the UK needs coordinated efforts between industry and government to capitalise on this global opportunity, and to maintain its position as a construction leader.

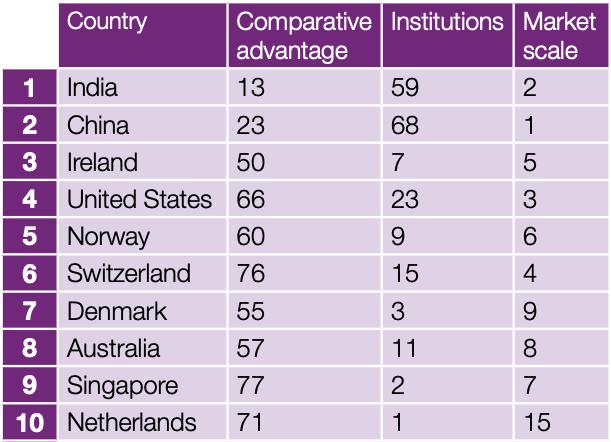

The Index

The Construction Partner Index ranks 78 countries based on their potential as partners and targets for the UK's construction industry. It assesses three pillars:

Institutions (legal systems, trade openness)

Market Scale (size of potential market)

Comparative Advantage (trading patterns, construction industry importance)

Factors like urbanisation and infrastructure quality are considered to determine the level of support needed from the construction sector in each country.

Top

India and China rank at the top of the Construction Partner Index due to their large market scale. India has surpassed China, with improved institutional performance and comparative advantage driven by growing urbanisation rates.

Five of the top ten countries in the index are from Western Europe, including Ireland, Norway, Switzerland, Denmark, and the Netherlands, benefiting from high-quality institutions and consistent high per-capita incomes.

Bottom

At the bottom of the index, Libya ranks 78th and Tunisia 77th due to recent political and economic instability. Other North African neighbours also rank low for similar reasons. I imagine that future reports will see the rise of African countries whose Comparative Advantage ranks high (see below), but is currently held back by instability and inferior institutions.

Several Eastern and Southern European countries, like Greece, Bulgaria, and Croatia are in the bottom quarter due to economic stagnation and shrinking populations reducing demand.

Movers

Over the past decade, the United Arab Emirates (UAE) and Lithuania have been the most improved countries, rising 28 and 27 places, respectively. The UAE's performance improved significantly on the market scale pillar due to economic restructuring and a focus on professional services. Lithuania's rise in the index was driven by improved institutions, reduced capital controls, and economic growth.

Bulgaria and Kazakhstan fell the most places, dropping 32 and 30 places, respectively, while Greece and Angola each dropped 23 places on the index.

Pillar by Pillar